Understanding the AICPA Code: A Practical Guide for Accountants

This guide provides actionable insights into the AICPA Code of Conduct, helping accounting professionals navigate ethical dilemmas and maintain the highest professional standards. Whether you're a seasoned CPA or just starting your career, understanding and applying this code is paramount for building a successful and ethical practice. Failure to comply can lead to significant penalties, including loss of license and reputational damage. The cornerstone of this code is the public interest; safeguarding the integrity of financial reporting is central to everything it encompasses.

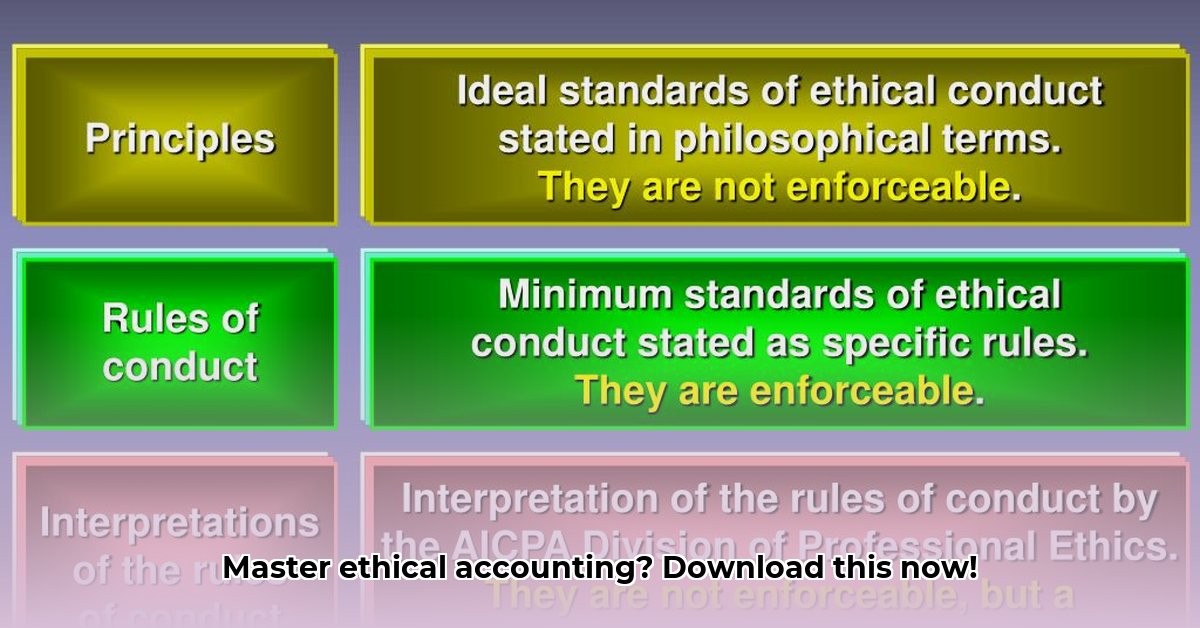

Core Principles: The Foundation of Ethical Accounting

The AICPA Code rests on five fundamental principles: Responsibilities, the Public Interest, Integrity, Objectivity, and Due Care.

Responsibilities: CPAs have a duty not only to their clients but also to the public, upholding the integrity of the financial system. This broad responsibility requires careful consideration of the impact of one's actions on all stakeholders.

Public Interest: Protecting the public interest is paramount. CPAs must prioritize the accuracy and reliability of financial information, ensuring its impact serves the common good. This is the guiding principle in all ethical deliberations.

Integrity: Honesty and straightforwardness are essential. CPAs must be trustworthy and transparent in their dealings, avoiding conflicts of interest and maintaining the highest ethical standards. Maintaining integrity builds trust and long-term success.

Objectivity: Impartiality is crucial when analyzing financial data. CPAs must avoid personal biases and ensure professional skepticism in all their work. Objectivity ensures that financial reports are free from personal influence.

Due Care: CPAs must maintain professional competence and diligence. Continuous learning and adherence to professional standards are necessary to perform quality work. Due care reflects commitment to excellence.

Navigating Ethical Dilemmas: A Step-by-Step Approach

Ethical dilemmas are inevitable in accounting. The AICPA Code provides a structured approach to resolving these challenges:

Identify the Ethical Issue: Clearly define the conflict and any potential violations of the Code. Accurate identification of the issue is the first step toward finding a solution.

Consult the Code: Refer to the relevant sections of the AICPA Code for guidance. The Code itself often provides solutions or points to the relevant professional actions.

Seek Advice: Consult with a mentor, supervisor, or ethics committee for an objective perspective. A second opinion can significantly help to clarify the situation.

Document Your Decision-Making Process: Maintain thorough records of your analysis, reasoning, and chosen actions. This meticulous documentation protects you against future challenges or questions.

Act Decisively: Make a well-informed decision, ensuring it aligns with the Code's principles and your ethical values. This concludes the process and establishes a precedent for the future.

Maintaining Independence: A Critical Element

Independence is crucial, particularly for auditors. The AICPA Code outlines strict guidelines for maintaining objectivity and avoiding conflicts of interest. The SEC's rules (for publicly traded companies) provide additional regulatory requirements. Maintaining independence requires a holistic and ongoing effort. It ensures public trust in the integrity of financial statements.

Data-backed rhetorical question: Do you know the percentage of audit failures directly linked to independence violations? A significant portion, highlighting the importance of this section.

Confidentiality: Protecting Sensitive Client Information

Protecting client confidentiality is a cornerstone of the profession. The AICPA Code strictly limits situations where confidential information can be disclosed. This includes legal obligations and specific instances of potential harm.

Quantifiable fact: The AICPA Code explicitly lists limited exceptions to confidentiality, emphasizing the gravity of its maintenance. This reinforces the seriousness of the confidentiality requirement.

Real-World Examples: Applying the AICPA Code

Let's consider a scenario: A client pressures you to manipulate financial figures. Following the AICPA Code, you would refuse, emphasizing the severity of such a breach of ethical accounting principles. Another example: Discovering suspicious activity in a client's accounts requires timely reporting through established channels, as dictated by the Code.

Human element (expert quote): "Maintaining ethical standards isn't just about avoiding legal trouble; it's about building trust and upholding the integrity of the profession," says Dr. Anya Sharma, Professor of Accounting Ethics at the University of California, Berkeley.

Continuous Professional Development: Staying Current

The accounting landscape is constantly evolving. Staying up-to-date on the AICPA Code and related regulations is vital. Regular professional development courses and continuing education help maintain ethical competencies and keep you compliant.

Conclusion: Embracing Ethical Accounting

The AICPA Code of Conduct is not merely a set of rules; it’s a commitment to ethical practice. By understanding and applying its principles, you enhance your professional reputation and contribute to the public good. This commitment extends beyond compliance and reflects a dedication to upholding the highest standards of professional conduct.